Chapter 1 Machine Learning for Social Scientists

Machine Learning practitioners and social scientists share many things in common. These shared traits are mostly related to the transformation, analysis and evaluation of statistical models. In fact, when many of my fellow social scientists take any introductory course on machine learning, I often hear that many of the things they get taught are very common in their social statistics classes. This is good news! This means that you already have a foot inside the field without even knowing it. Machine Learning practitioners use many of the same statistical model we use and also many of transformation techniques that we use. However, there are important differences on how we analyze data and how we answer our questions. In this chapter I will elaborate on how machine learning practitioners have developed strategies different from social scientists for analyzing their data, how their analysis workflow compares to ours and finally, a tour around their way of thinking, which has evolved to be very different from ours.

I hope that by understanding the strategies and techniques that machine learning practitioners use, social scientists would expand their analysis toolbox, allowing us to complement their way of thinking with our strong research design skills and modeling techniques.

1.1 A different way of thinking

The first question we want to ask ourselves is, what is machine learning? Machine Learning bears indeed a fancy name which brings to mind thoughts related to artificial intelligence and robots. However, as you’ll see throughout the course, most terms and models used in machine learning are actually what we know as statistical models. The overarching difference in the definition of machine learning and social statistics is not the models or new strategies for analyzing data. It is the main objective of the analysis. What is machine learning after all?

Using statistical methods to learn the data enough to be able to predict it accurately on new data

That sounds somewhat familiar to us social scientists. Perhaps our goal is not to predict our data but it is certainly to learn it and understand it. In particular, social scientists are interested in figuring out if our theoretical description of a problem fits the data we have collected or have at hand. We do that by carefully building a model that explains the problem really well such that we can extrapolate an explanation for the problem from the data. Our gold standard to check whether we did a good job is to collect the exact same data again and see if our final models replicates. How does this differ from the way of thinking of machine learning practitioners? The main objective in a machine learning problem is accurate predictions; that is, regardless of how well they understand a problem, they want to learn the data enough to predict it well. Prediction problems are usually concerned with building and tweaking a model that predicts a dependent variable accurately on your data, such that when new data arrives, the model can predict it just as accurately. This does not mean that machine learning practitioners don’t have domain-specific knowledge of what they’re trying to predict (they have to select variables to include in a model just as we do). However, ‘parsimonious models’ (that is, simple and interpretable models) are not something they’re limited to (in contrast, social scientists hardly experiment with non-interpretable models). They might use models which contain up to hundreds of variables if that increases predictive accuracy. Although that might sound counter-intuitive to social scientists, more and more ground is being gained by this type of thinking in the social sciences (Watts 2014; Yarkoni and Westfall 2017).

The difference between how we both approach research questions is the problem of inference versus prediction (Breiman and others 2001). That is the fundamental difference between the approach used by social scientists and practitioners of machine learning. However, for having such drastic differences in our objective, we share a lot of common strategies. For example, here’s the typical workflow of a social scientist:

This is our safe zone: we understand these steps and we’ve exercised them many times. We begin by importing our data and immediately start to clean it. This involves, for example, collapsing fine grained groups into bigger categories, transforming variables using logarithms and creating new variables which reflect important concepts from our theoretical model. Once we’re confident with our set of variables, we begin the iterative process of visualizing our data, fitting statistical models and evaluating the fit of the model. This is an iterative process because the results of our model might give us ideas on new variables or how to recode an existing variable. This prompts us to repeat the same process again with the aim of carefully building a model that fits the data well. Well, let me break it to you but this same process is very familiar to the machine learning process:

They import their data, they wrangle their data, they fit statistical models, and they evaluate the fit of their models. They might have different names for the same things but in essence, they are more or less the same. For example, here are some common terms in the machine learning literature which have exact equivalents in social statistics:

- Features –> Variables

- Feature Engineering –> Creating Variables

- Learning Algorithms –> Statistical Models

- Supervised Learning –> Models that have a dependent variable

- Unsupervised Learning –> Models that don’t have a dependent variable, such as clustering

- Classifiers –> Models for predicting categorical variables, such as logistic regression

and you’ll find more around. These are the common steps which you’ll find between both fields. However, machine learning practitioners have developed extra steps which help them achieve their goal of predicting new data well:

- Training/Testing data –> Unknown to us

- Cross-validation –> Unknown to us

- Grid search –> Unknown to us

- Loss functions –> Model fit –> Known to us but are not predominant (\(RMSE\), \(R^2\), etc…)

These are very useful concepts and we’ll focus on those in this introduction. In this introduction I won’t delve into the statistical models (learning algorithms) used in machine learning as these will be discussed in later chapters but I wanted to highlight that although they share similarities with the models used in social statistics, there are many models used in the machine learning literature which are unknown to us. Let’s delve into each of these three new concepts.

Before we beginning explaining these concepts and using R, let’s load the packages we’ll use in this chapter:

1.2 Split your data into training/testing

Since the main objective in machine learning is to predict data accurately, all of their strategies are geared towards avoiding overfitting/underfitting the data. In other words, they want to capture all the signal and ignore the noise:

## Data creation

set.seed(2313)

n <- 500

x <- rnorm(n)

y <- x^3 + rnorm(n, sd = 3)

age <- rescale(x, to = c(0, 100))

income <- rescale(y, to = c(0, 5000))

age_inc <- data.frame(age = age, income = income)

## Data creation

y_axis <- scale_y_continuous(labels = dollar_format(suffix = "€", prefix = ""),

limits = c(0, 5000),

name = "Income")

x_axis <- scale_x_continuous(name = "Age")

bad_fit <-

ggplot(age_inc, aes(age, income)) +

geom_point() +

geom_smooth(method = "lm") +

y_axis +

x_axis +

ggtitle("Underfit") +

theme_linedraw()

overfit <-

ggplot(age_inc, aes(age, income)) +

geom_point() +

geom_smooth(method = "loess", span = 0.015) +

y_axis +

x_axis +

ggtitle("Overfit") +

theme_linedraw()

goodfit <-

ggplot(age_inc, aes(age, income)) +

geom_point() +

geom_smooth(method = "loess", span = 0.9) +

y_axis +

x_axis +

ggtitle("Ideal fit") +

theme_linedraw()

bad_fit + overfit + goodfit

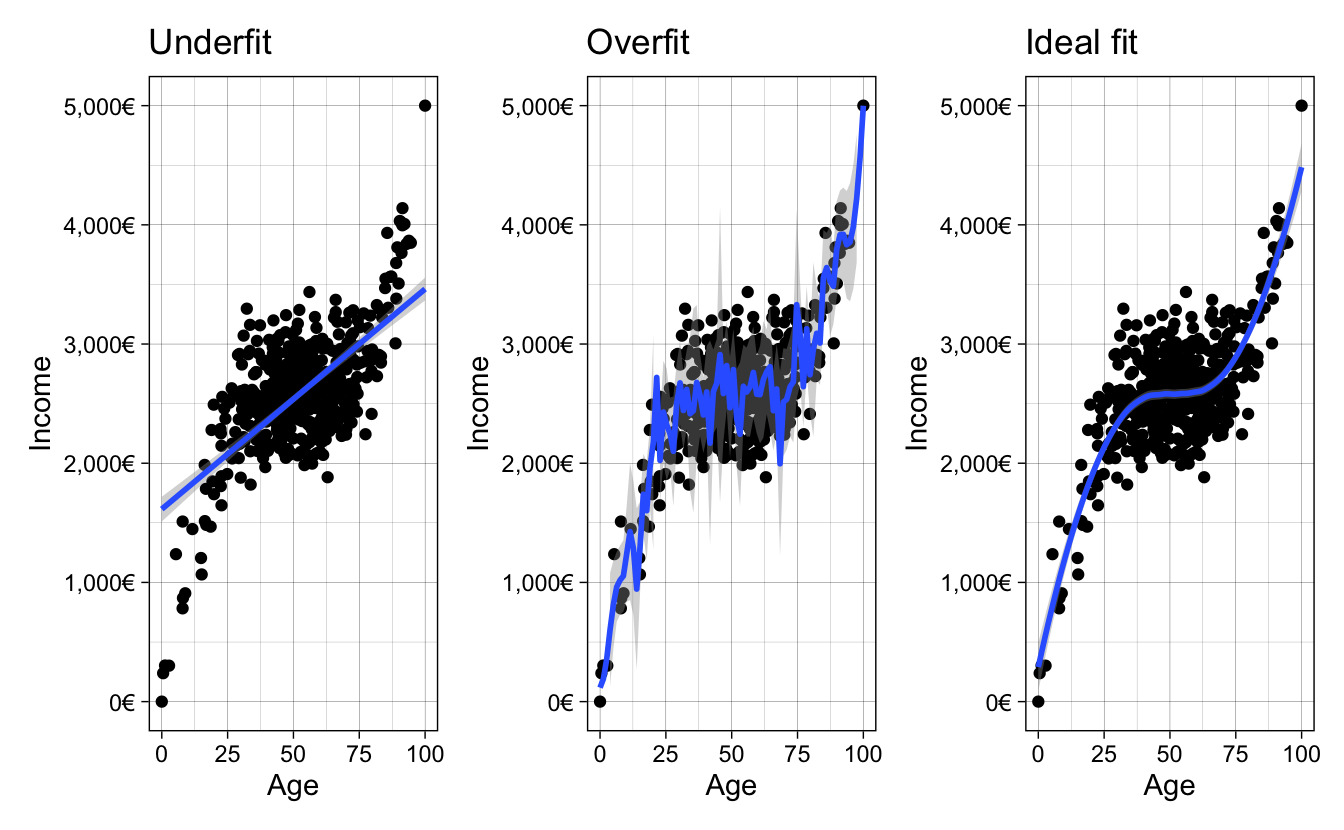

Figure 1.1: Different ways of fitting your data

The first panel of figure 1.1 shows a model which is not flexible, as it fits a straight line without capturing the subtle non-linearities of the data. The middle panel is too flexible as it captures much of the random noise of the non-linear relationship. Finally, the third panel shows the ideal fit, where the fitted line is flexible enough to capture the non-linear relationship in the data yet it it is mainly unaffected by the random noise in the data. Although social scientists are aware of these concepts, we really don’t think about them a lot. When we perform statistical modeling we don’t really think about whether we’re overfitting or underfitting: we’re mostly paying attention to whether the statistical relationships make sense.

For example, how would social scientists fit a model? They would take the entire data

and fit the model on it. How do you know you’re overfitting? Well, one very easy and naive approach is to randomly divide your data into two chunks called training and testing:

The training data usually consists of a random sample of around ~70% of the initial data and the testing data the remaining ~30% of the initial data. If a particular row is in the training data, it must not be on the testing data. In contrast, if a particular row is in the testing data, it shouldn’t be in the training data either. Why should splitting the data into two chunks help us fix the problem of overfitting? Because you can elaborate your model in the training set as much as you want, and when you’re confident enough, the testing data can serve as an unseen, pristine source of data on which you can evaluate your model. If fitting your model on the testing data shows that your model was too optimistic, you were probably overfitting the data.

Let’s go through the steps one by one. Fit your model in the training data (remember, that’s a random sample of about 70% of the initial data)

evaluate the model fit and make the same changes you would do on your complete data: create new variables, recode variables, etc. You can think of this chunk as the complete data to perform your analysis. It is the equivalent of the initial data where social scientists fit their models. Once you’re very comfortable with your model, the best recipe for checking whether your model was overfitting is to use this fitted model to predict on the other chunk of data (the testing data):

If you tweaked your model in such a way that it learned the noise of your training data, it will perform poorly on the testing data, since your the model didn’t capture the overall trend in the training data but rather the noise.

It’s time to introduce how we perform these steps in R. For this, we’ll use the package tidyflow, a package created for this book. It aims to have a simple and intuitive workflow for machine learning which you’ll learn through this book. You can install the package with the code below:

In R we can build a machine learning ‘workflow’ with the function tidyflow. To this workflow, we can plug in steps that you can execute. In our example, to plug in the step of partitioning the data into training and testing, you can use plug_split with the function initial_split:

library(tidyflow)

ml_flow <-

age_inc %>%

tidyflow(seed = 2313) %>%

plug_split(initial_split)

ml_flow## ══ Tidyflow ════════════════════════════════════════════════════════════════════

## Data: 500 rows x 2 columns

## Split: initial_split w/ default args

## Recipe/Formula: None

## Resample: None

## Grid: None

## Model: Nonetidyflow already knows that age_inc is the main data source and that we need to apply the training/testing split with initial_split. You can think of this as plan that will be executed once you tell it to.

Let’s get back to our example and suppose that you fit your model several times on the training data, tweaking it to improve performance (when I say tweaking I mean applying transformations, including new variables, recoding old variables, including polynomials, etc..). When you think you’re ready, you use this model to predict on the testing data and find out that the model was indeed overfitting the data because you cannot predict the testing data as well as the training data. You then go back to the training data, tweak some more, run some models again and when you think the model is ready again, you predict on your testing data again and find that it improved. Then you repeat the process again, \(3\), \(4\), \(5\) \(N\) times. If you do that, you will, in very subtle ways, start to overfit your model on the testing data! In other words, you’re fitting a model \(N\) times on your training data, evaluating its fit on the testing data and then tweaking again to improve the prediction on the testing data. The testing data should serve as the final dataset to compare your model: you should not tweak the model again after seeing how your model fits the unseen testing data.

That doesn’t sound right. It seems we have too few “degrees of freedom” to test the accuracy of our model. We can tweak the model in the training data as much as we want but we only have one attempt at testing our model against the testing data. How can we evaluate, then, whether we’re overfitting with the training data alone, then? Enter cross-validation

1.3 Cross-validation

The idea behind cross-validation is to allow the user to check whether they’re overfitting the data without predicting on the testing data. How does it work? First, we only work with our training data

and replicate the training data 10 times

The 10 rectangular red rows below the training data, contain an exact replica of the initial training data. That is, if the initial training data has 500 rows and 10 columns, then each of these red rectangled rows also has 500 rows and 10 columns. The idea behind this approach is that for each rectangled row, you can use 70% of the data to fit your model and then predict on the remaining 30%. For example, for the first rectangled row, you would fit your initial model model with some tweak (let’s say, adding a squared term to the age variable to check if that improves fit) on the training data and then predict on the testing data to evaluate the fit:

Since we fit a model to the trainingdata of each rectangled row and then predict on the testing data of each rectangled row, we can record how well our model is doing for each of our replicate data sets. For example, for the first row we record the \(RMSE\) of the prediction on the testing data. For the second rectangled row, fit the exact same model (that is, including the age squared term) on 70% of the training data, predict on the testing data and record the \(RMSE\). And then repeat the same iteration for every rectangled row:

After you’ve fitted the model and evaluated the model 10 times, you have 10 values of the \(RMSE\). With these 10 values you can calculate the average \(RMSE\) and standard error of your model’s performance.

Note that with this approach, the testing data changes in each rectangled row, making sure that each ~30% chunk of the data passes through the testing dataset at some point during the predictions. This is done to ensure the predictions are as balanced as possible.

This approach offers a way to iterate as many times as you want on tweaking your model and predicting on the cross-validated testing data without actually predicting on the initial testing dataset. This is the least bad approach that is currently accepted in the literature.

Why is it the least bad approach? Because if we tweak the model on these 10 replicas one time, then a second time, then a third time, etc…, we’ll also start overfitting on each of these 10 slots! The superiority of this approach over tweaking on the training data is that since we have 10 replicas, we can take the average of model fit metrics and also obtain standard errors. This allows to have a somewhat balanced account of how our model fit is doing and the uncertainty around it.

That said, since we will always overfit in someway using a cross-validation approach, the final error of your model fit on the training data will always be over optimistic (lower error than what you will actually have, if you predicted on the pristine testing data.

Based on our previous tidyflow, we can plug in a cross-validation step with plug_resample. There are many different cross-validation techniques but let’s focus on the one from our example (replicating the data 10 times). For that, we use the function vfold_cv:

## ══ Tidyflow ════════════════════════════════════════════════════════════════════

## Data: 500 rows x 2 columns

## Split: initial_split w/ default args

## Recipe/Formula: None

## Resample: vfold_cv w/ default args

## Grid: None

## Model: None1.4 Bias-Variance Tradeoff

Before we elaborate a complete coded example, it’s important to talk about the concept of bias-variance tradeoff used in machine learning problems. As was shown in figure 1.1, we want the ideal fit without overfitting or underfitting the data. In some instances, fitting the data that well is very difficult because we don’t have variables that reflect the data generating process or because the relationship is too complex. In that case, for machine learning problems, you might want to either underfit or overfit slightly, depending on your problem.

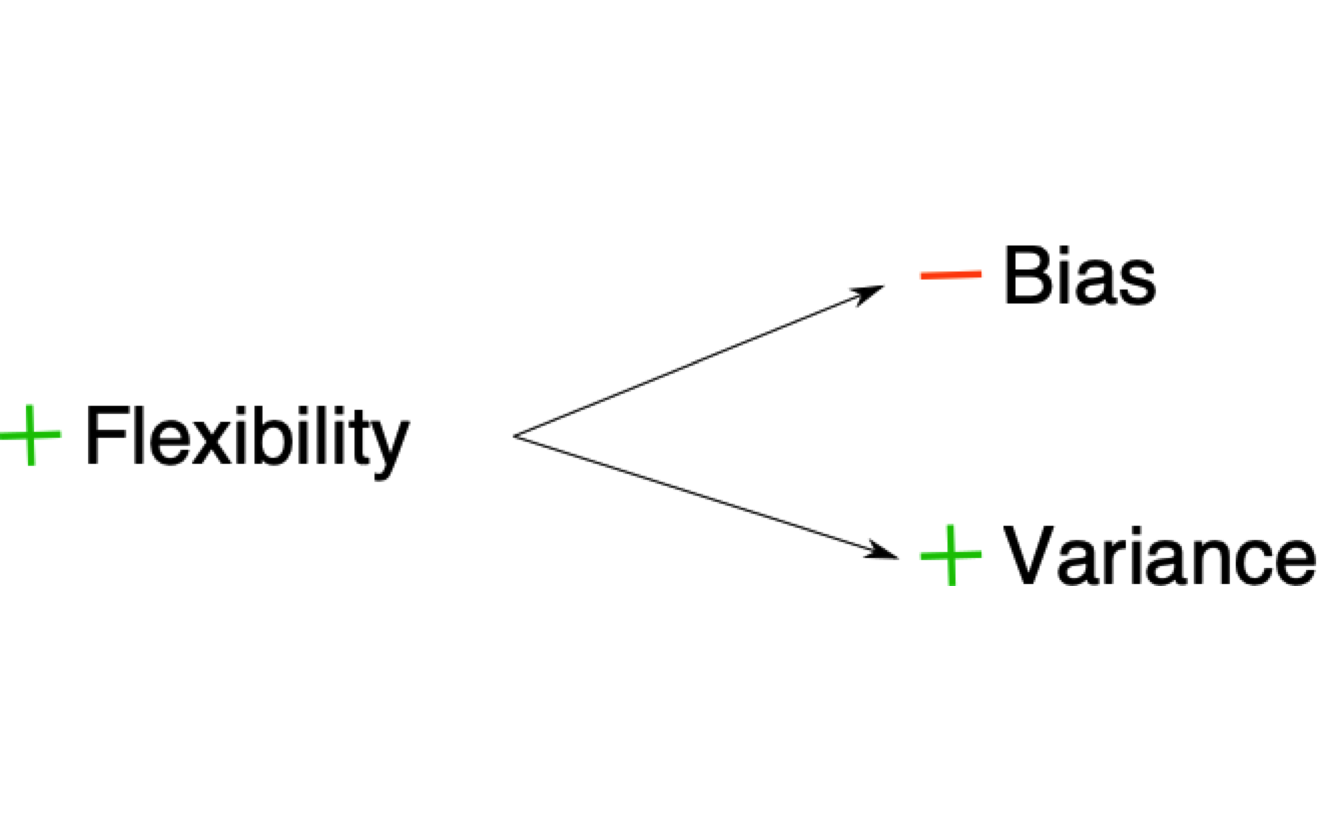

Overfitting your data has some value, which is that we learn the data very well. This is often called a model with a lot of flexibility. A model that can learn all the small intricacies of the data is often called a flexible model. There is very little bias in a model like this one, since we learn the data very very well. However, at the expense of bias, overfitting has a lot of variance. If we predict on a new dataset using the overfitted model, we’ll find a completely different result from the initial model. If we repeat the same on another dataset, we’ll find another different result. That is why models which can be very flexible are considered to have very little bias and a lot of variance:

The model above fits the criteria:

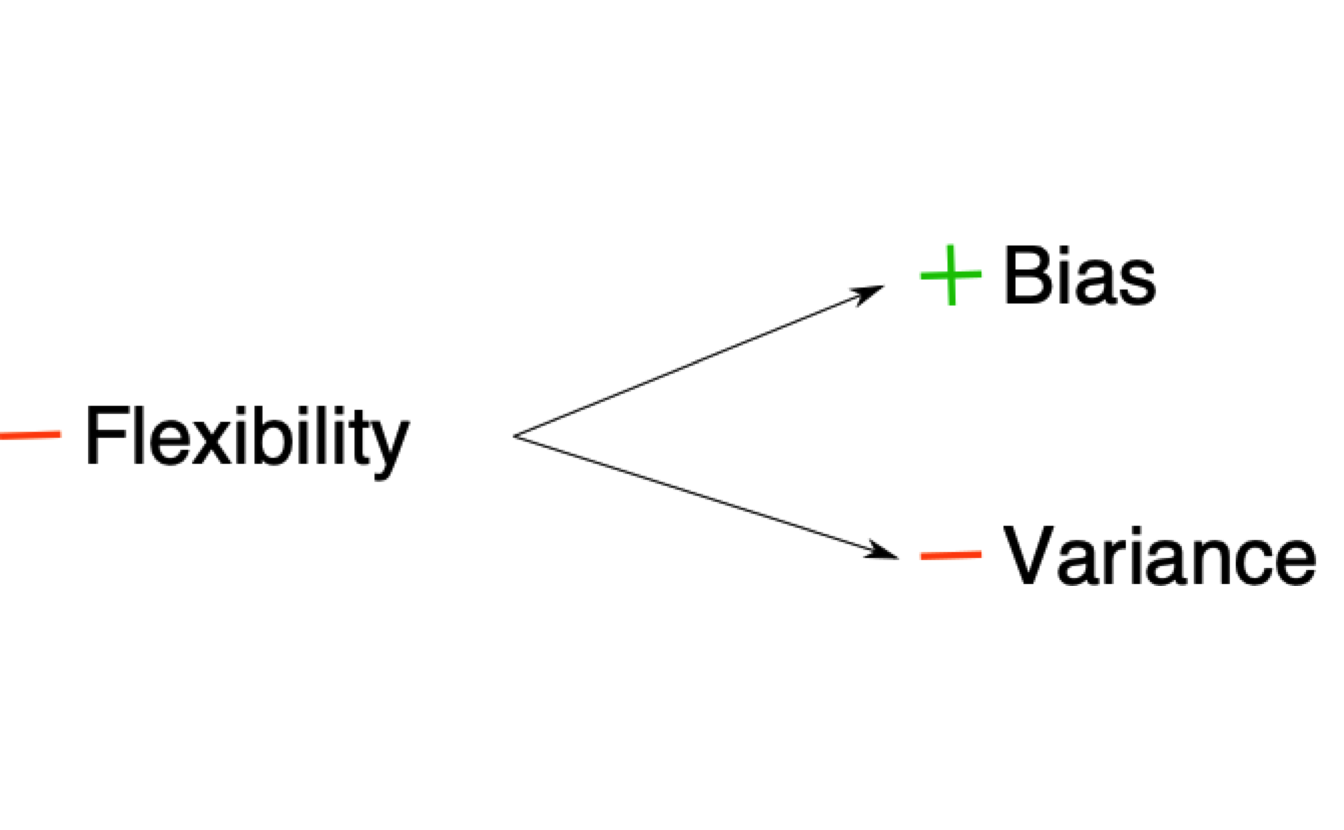

On the other hand, models which are not flexible, have more bias and less variance. One familiar example of this is the linear model. By fitting a straight line through the data, the variance is very small: if we run the same exact model on a new data, the fitted line is robust to slight changes in the data (outliers, small changes in the tails of the distribution, etc..). However, the fitted line doesn’t really capture the subtle trends in the data (assuming the relationship is non-linear, which is in most cases). That is why non-flexible models are often called to have high bias and low variance:

or in other words:

In reality, what we usually want is something located in the middle of these two extremes: we want a model that is neither too flexible that overfits the data nor too inflexible that misses the signal. There is really no magical recipe to achieving the perfect model and our best approach is to understand our model’s performance using techniques such as cross-validation to assess how much our model is overfitting/underfitting the data. Even experienced machine learning practitioners can build models that overfit the data considerably (one notable example are the results from the Fragile Families Challenge, which tried to predict life outcomes using machine learning and ended up overfitting the data a lot. See Salganik et al. (2020)).

1.5 An example

Let’s combine all the new steps into a complete pipeline of machine learning in R. Let’s use the data age_inc which has the age of a person and their income. We want to predict their income based on their age. Let’s load the data and the packages of interest:

library(tidymodels)

library(tidyflow)

## Generate the data

rescale <- function(x, to = c(0, 1), from = range(x, na.rm = TRUE, finite = TRUE)) {

(x - from[1])/diff(from) * diff(to) + to[1]

}

set.seed(2313)

n <- 500

x <- rnorm(n)

y <- x^3 + rnorm(n, sd = 3)

age <- rescale(x, to = c(0, 100))

income <- rescale(y, to = c(0, 5000))

age_inc <- data.frame(age = age, income = income)

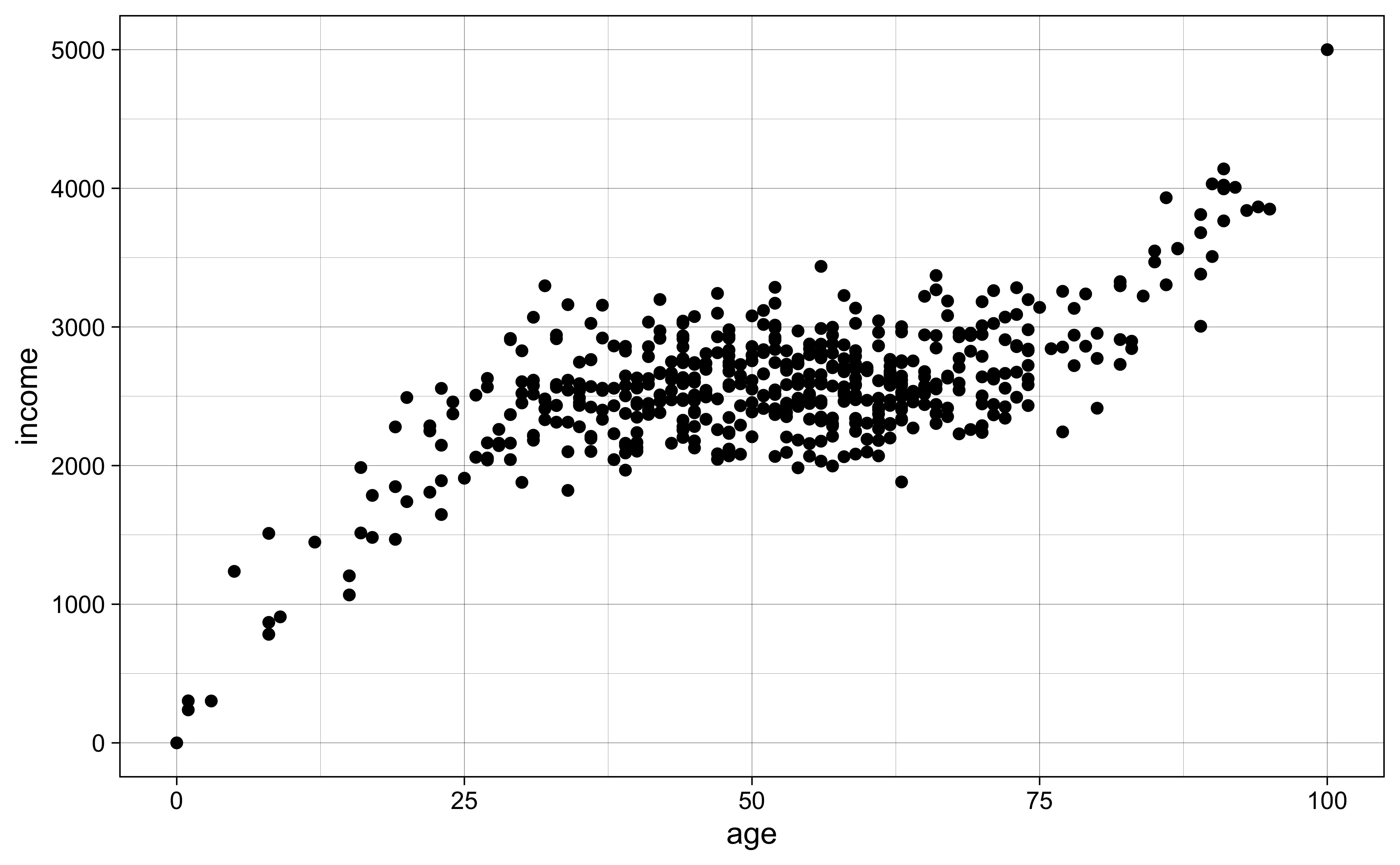

## End generate dataThis is how the data looks like:

The relationship between these two variables is non-linear, showing a variant of the Mincer equation (Mincer 1958) where income is a non-linear function of age:

# age_inc was defined above, and it is reused here

age_inc %>%

ggplot(aes(age, income)) +

geom_point() +

theme_linedraw()

Let’s construct our tidyflow and add a split with plug_split. This will separate the data into training and testing:

## ══ Tidyflow ════════════════════════════════════════════════════════════════════

## Data: 500 rows x 2 columns

## Split: initial_split w/ default args

## Recipe/Formula: None

## Resample: None

## Grid: None

## Model: NoneLet’s begin running some models. The first model we’d like run is a simple regression income ~ age on the training data and plot the fitted values.

# Run the model

m1 <-

ml_flow %>%

plug_recipe(~ recipe(income ~ age, data = .)) %>% # Add the formula

plug_model(linear_reg() %>% set_engine("lm")) %>% # Define the linear regression

fit() # Fit model

# Predict on the training data

m1_res <-

m1 %>%

predict_training()

m1_res## # A tibble: 375 x 3

## age income .pred

## <dbl> <dbl> <dbl>

## 1 57 2574 2652.

## 2 39 2091 2301.

## 3 63 2328 2769.

## 4 85 3548 3199.

## 5 65 2440 2808.

## 6 94 3866 3374.

## 7 8 1511 1696.

## 8 78 3134 3062.

## 9 56 2777 2633.

## 10 42 2918 2359.

## # … with 365 more rowsThe result of predict_training is the training data from age_inc with one new column: the predicted values of the model. Let’s visualize the predictions:

# Visualize the result

m1_res %>%

ggplot(aes(age, income)) +

geom_line(aes(y = .pred), color = "red", size = 2) +

geom_point() +

scale_x_continuous(name = "Age") +

scale_y_continuous(name = "Income",

label = dollar_format(suffix = "€", prefix = "")) +

theme_linedraw()

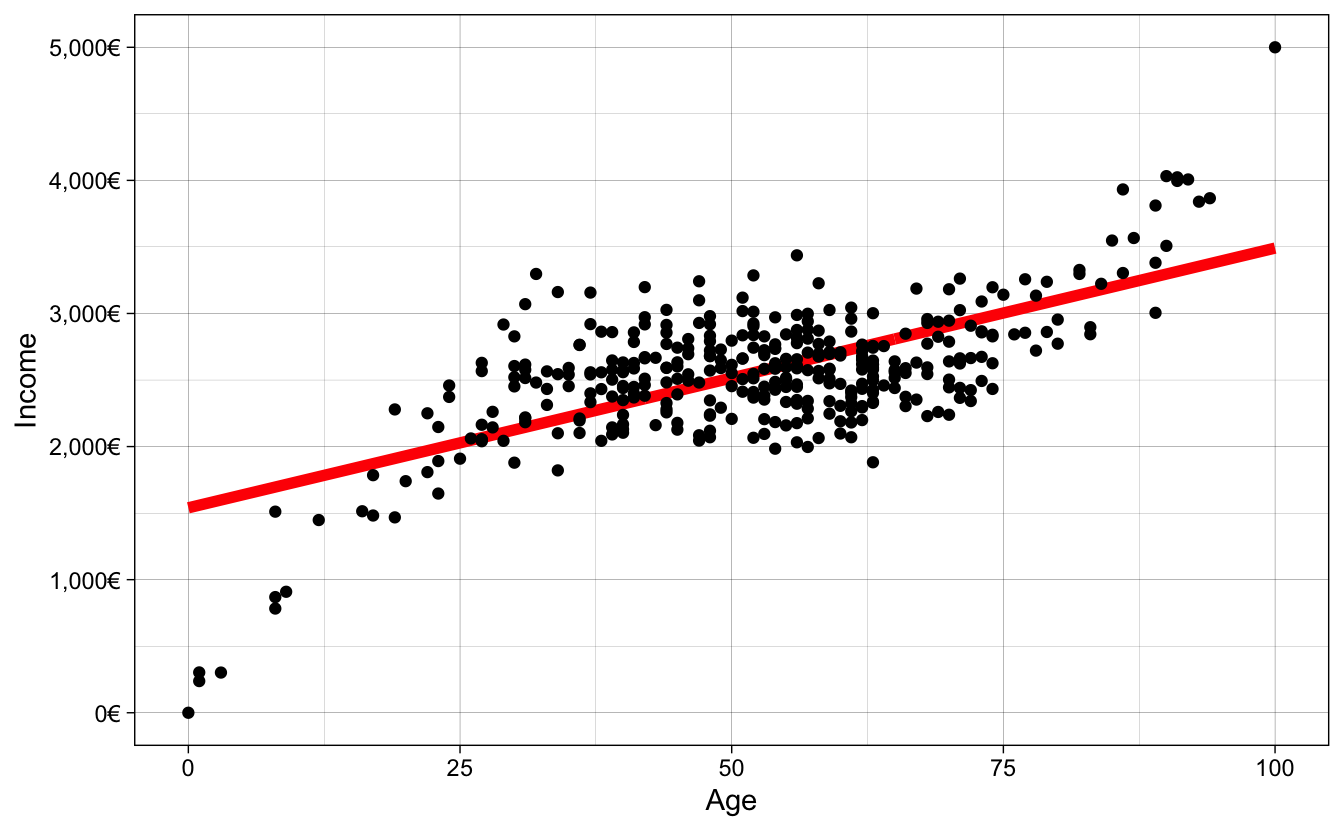

It seems we’re underfitting the relationship. To measure the fit of the model, we’ll use the Root Mean Square Error (RMSE). Remember it?

\[ RMSE = \sqrt{\sum_{i = 1}^n{\frac{(\hat{y} - y)^2}{N}}} \]

Without going into too many details, it is the average difference between each dot from the plot from the value same value in the fitted line. The current \(RMSE\) of our model is 380.56. This means that on average our predictions are off by around 380.56 euros. The fitted line is underfitting the relationship because it cannot capture the non-linear trend in the data. How do we increase the fit? We could add non-linear terms to the model, for example \(age^2\), \(age^3\), …, \(age^{10}\).

However, remember, by fitting very high non-linear terms to the data, we might get lower error from the model on the training data but that’s because the model is learning the training data so much that it starts to capture noise rather than the signal. This means that when we predict on the unseen testing data, our model would not know how to identify the signal in the data and have a higher \(RMSE\) error. How can we be sure we’re picking the best model specification?

This is where cross-validation comes in!

We can use the function vfold_cv to separate the training data into 10 cross-validation sets, where each one has a training and testing data.

## # 10-fold cross-validation

## # A tibble: 10 x 2

## splits id

## <list> <chr>

## 1 <split [337/38]> Fold01

## 2 <split [337/38]> Fold02

## 3 <split [337/38]> Fold03

## 4 <split [337/38]> Fold04

## 5 <split [337/38]> Fold05

## 6 <split [338/37]> Fold06

## 7 <split [338/37]> Fold07

## 8 <split [338/37]> Fold08

## 9 <split [338/37]> Fold09

## 10 <split [338/37]> Fold10Each of those split objects (there are 10) contains a training and testing set. This is the equivalent of the image we saw before:

The next thing we have to do is train the same model on the training data of each of these cross-validated sets, use these trained models to predict on the 10 testing sets and record the error rate using our \(RMSE\) metric. But don’t worry, you don’t have to do that all of that manually, tidyflow can leverage many packages to do that for you:

# Define the formula of your model and specify that the polynomial

# value will be 'tuned'. That is, we will try several values

# instead of only one.

rcp <-

~ recipe(income ~ age, data = .) %>%

step_poly(age, degree = tune())

m2 <-

m1 %>%

# Add the cross-validation step

plug_resample(vfold_cv) %>%

# Replace the initial recipe with the one with several polynomials

replace_recipe(rcp) %>%

# Here we define the values we will try, from 2 to 10

plug_grid(expand.grid, degree = 2:10) %>%

# Fit the model

fit()

# Visualize the result

m2 %>%

pull_tflow_fit_tuning() %>% # Extract all models with different 'degree' values

autoplot() +

theme_linedraw()

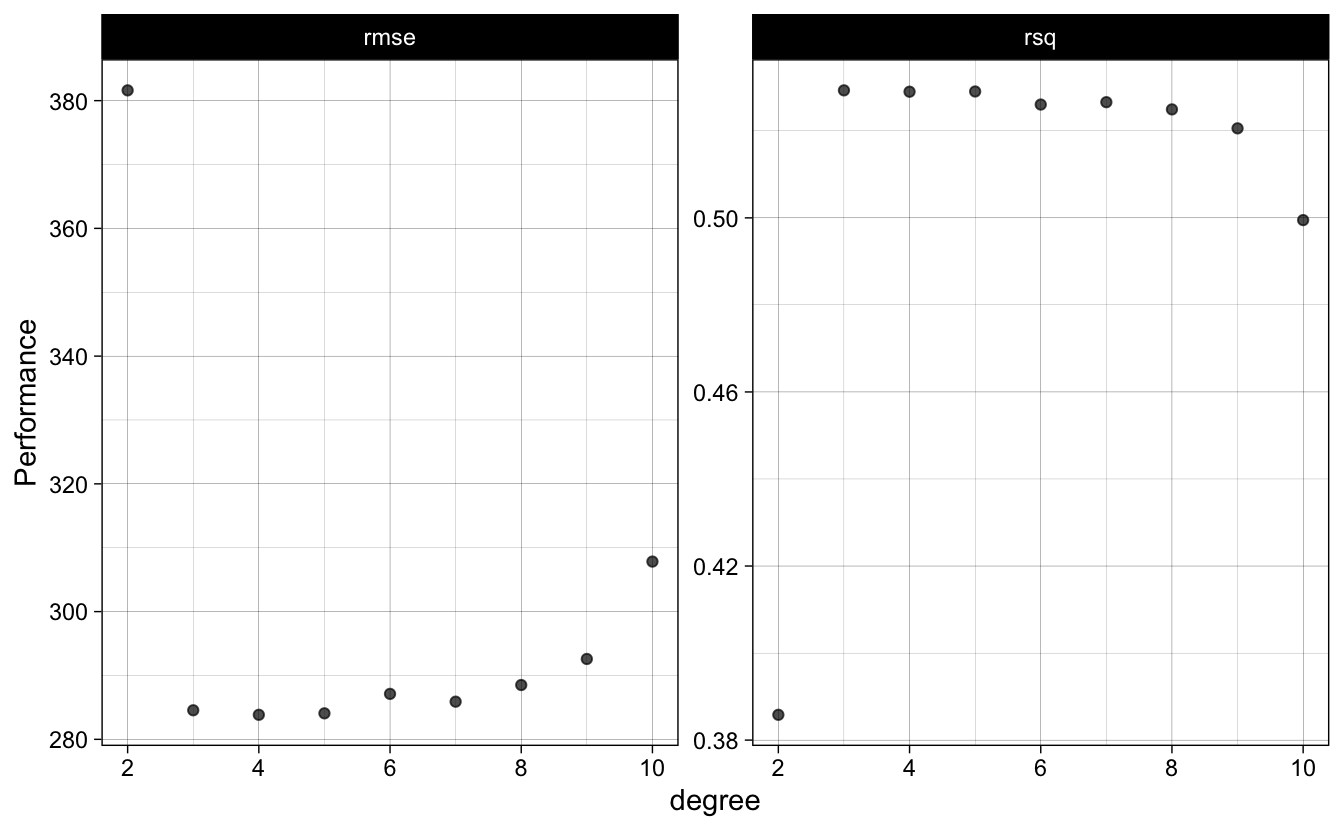

Figure 1.2: Average evaluation metrics of predicting on the testing data through the 10 cross-validation sets

Figure 1.2 shows the error rate for the \(RMSE\) and the \(R^2\). For the \(RMSE\) (left panel), the resulting error terms show that any polynomial above 2 has very similar error rates. However, there is a point in which adding \(age^9\) and \(age^{10}\) increases the error rate. This decrease in fit as complexity increases can also been see with the \(R^2\) (right panel), as it decreases with higher polynomials. This is a good example where a lot of flexibility (fitting the non-linear trend very well), increases accuracy on the training set but shows a lot variability on the testing set. The \(RMSE\) that we see in figure 1.2 is the average \(RMSE\) from predicting on the testing set using the model fitted on the training data in the 10 cross validated sets.

Given that most of the polynomial terms have similar error terms, we usually would go for the simplest model, that is, the model with \(age^3\). We can run the model on the entire training data with 3 non-linear terms and check the fit:

# Fit the final model with degrees = 3

res_m2 <- complete_tflow(m2, best_params = data.frame(degree = 3))

res_m2 %>%

predict_training() %>%

ggplot(aes(age, income)) +

geom_line(aes(y = .pred), color = "red", size = 2) +

geom_point() +

scale_x_continuous(name = "Age") +

scale_y_continuous(name = "Income",

label = dollar_format(suffix = "€", prefix = "")) +

theme_linedraw()

The \(RMSE\) on the training data for the three polynomial model is 280.47. We need to compare that to our testing \(RMSE\).

res_m2 %>%

predict_testing() %>%

ggplot(aes(age, income)) +

geom_line(aes(y = .pred), color = "red", size = 2) +

geom_point() +

scale_x_continuous(name = "Age") +

scale_y_continuous(name = "Income",

label = dollar_format(suffix = "€", prefix = "")) +

theme_linedraw()

- training \(RMSE\) is 280.47

- testing \(RMSE\) is 312.29

testing \(RMSE\) will almost always be higher, since we always overfit the data in some way through cross-validation.

References

Breiman, Leo, and others. 2001. “Statistical Modeling: The Two Cultures (with Comments and a Rejoinder by the Author).” Statistical Science 16 (3): 199–231.

Mincer, Jacob. 1958. “Investment in Human Capital and Personal Income Distribution.” Journal of Political Economy 66 (4): 281–302. https://doi.org/10.1086/258055.

Salganik, Matthew J, Ian Lundberg, Alexander T Kindel, Caitlin E Ahearn, Khaled Al-Ghoneim, Abdullah Almaatouq, Drew M Altschul, et al. 2020. “Measuring the Predictability of Life Outcomes with a Scientific Mass Collaboration.” Proceedings of the National Academy of Sciences 117 (15): 8398–8403.

Watts, Duncan J. 2014. “Common Sense and Sociological Explanations.” American Journal of Sociology 120 (2): 313–51.

Yarkoni, Tal, and Jacob Westfall. 2017. “Choosing Prediction over Explanation in Psychology: Lessons from Machine Learning.” Perspectives on Psychological Science 12 (6): 1100–1122.